Corporate Sustainability Reporting Directive (CSRD)

In a world where sustainability is increasingly central to our collective agenda, European regulators have taken a significant step towards making companies more responsible for their environmental, social and governance (ESG) impacts. The Corporate Sustainability Reporting Directive (CSRD) is the latest instrument driving this change, stemming from the vision of the EU Green Deal.

The introduction of the CSRD amends the 2013 European Accounting Directive and replaces the Non-Financial Reporting Directive. The CSRD builds on the foundation laid by the NFRD and stems from the growing recognition that companies need to do more than just make profits. In an era of climate change, social inequality and changing stakeholder expectations, investors and the public have a greater need for ESG transparency.

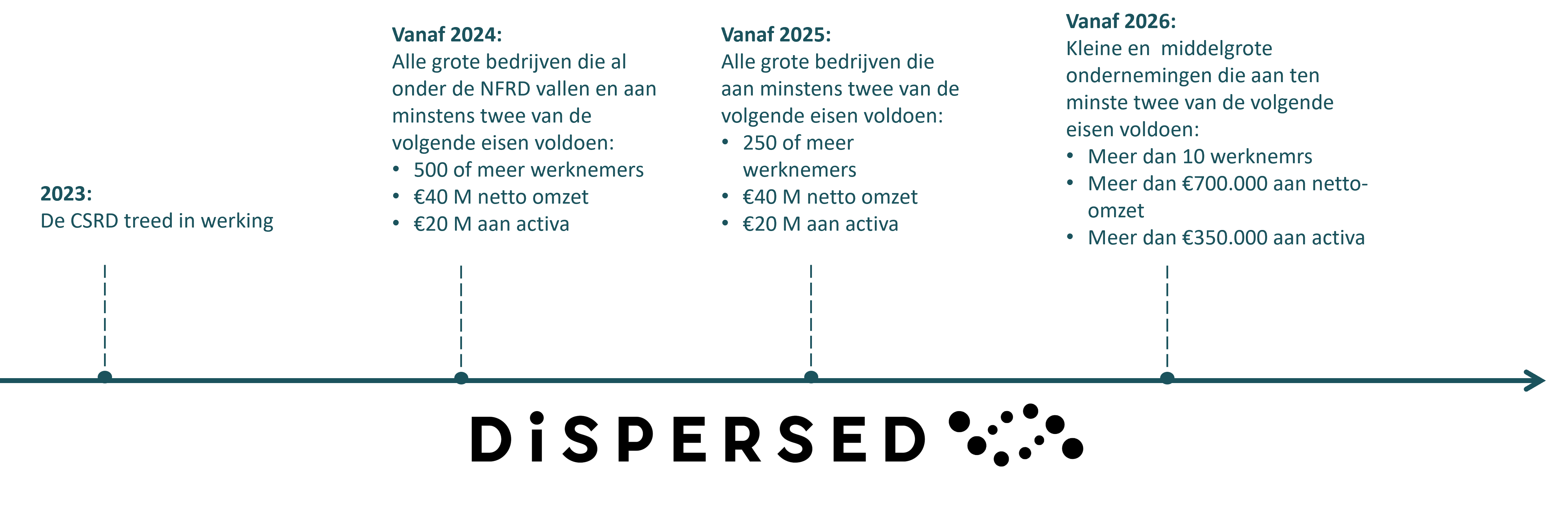

These new regulations will force companies to report more thoroughly and consistently on their sustainability efforts. Initially, the CSRD will take effect for large publicly traded companies, but a reduced version of will also be introduced for SMEs later. The goal is to provide stakeholder with reliable and comparable information that takes a holistic view of organizations' sustainability performance. The timeline below illustrates the implementation of the directive.

As shown in the timeline above, the CSRD will initially apply to large companies before it will apply to listed SMEs starting in 2026. This means that small and medium-sized listed companies will have to be "CSRD-ready" by 2025 and start preparing for the CSRD as early as 2024. Despite the fact that the CSRD will not officially apply to unlisted SMEs, the directive is still expected to have implications for these companies.

SMEs will start to feel pressure from larger customers and suppliers to meet stricter sustainability standards. Moreover, financial stakeholders such as investors and lenders may demand CSRD compliance, while consumer demand for sustainable products is expected to increase as well. This will further increase pressure on unlisted companies to report on ESG topics. The CSRD will thus cause a domino effect, so to speak, with regard to sustainability transparency. All the more reason, therefore, even as an SME that is not required to report, to keep an eye on developments and prepare adequately for the implementation of the CSRD.

So we now know when the CSRD will take effect, and to whom it will apply. What exactly is expected of you now? Fair question. To answer this question, 12 guiding principle have been developed: the European Sustainability Reporting Standards (ESRS). These ESRS state what must be reported, and in what way. In this way, the ESRS provides practical substance to the concepts of CSRD.

The general principles are set forth in ESRS 1 and 2. Companies subject to CSRD are required to report according to the general requirements of ESRS 1 and 2. In addition, ten specific ESRS have been published, covering specific ESG topics such as climate change, pollution, biodiversity, as well as employees in the value chain or business behavior. The image below provides an overview of these ten ESRS.

At Dispersed, we understand the importance of these changes and help companies take the right steps toward a more sustainable future. For most companies the initial focus of CSRD activities will center around the Environmental component. Our Scope 1-2-3 and Impact Assessments are powerful tools that offer organizations insight into the environmental impacts of their products, services or operations.

These assessments provide the starting point for defining strategies toward net-zero emissions. A net-zero roadmap, based on the principles of the Science-Based Targets Initiative (SBTi), provides a clear pathway to significantly reduce carbon emissions and align with global climate goals.

Every company is unique, which is why we offer customized net-zero strategies that provide concrete tools to become more sustainable. By basing our strategies on thorough impact analyses, we can always identify the most impactful reduction actions.

Once on the journey to sustainability, we also help obtain relevant sustainability labels and certifications. These labels are a powerful way to make your organization's sustainability efforts visible to stakeholders. At Dispersed, we believe that the path to sustainable business practices begins with insight and is followed by action. Our approach enables companies not only to comply with upcoming CSRD regulations, but also to actively contribute to a more sustainable future.

Want to learn more about the CSRD, or do you have a specific question about the solutions we offer? Then make an appointment with one of our specialists.